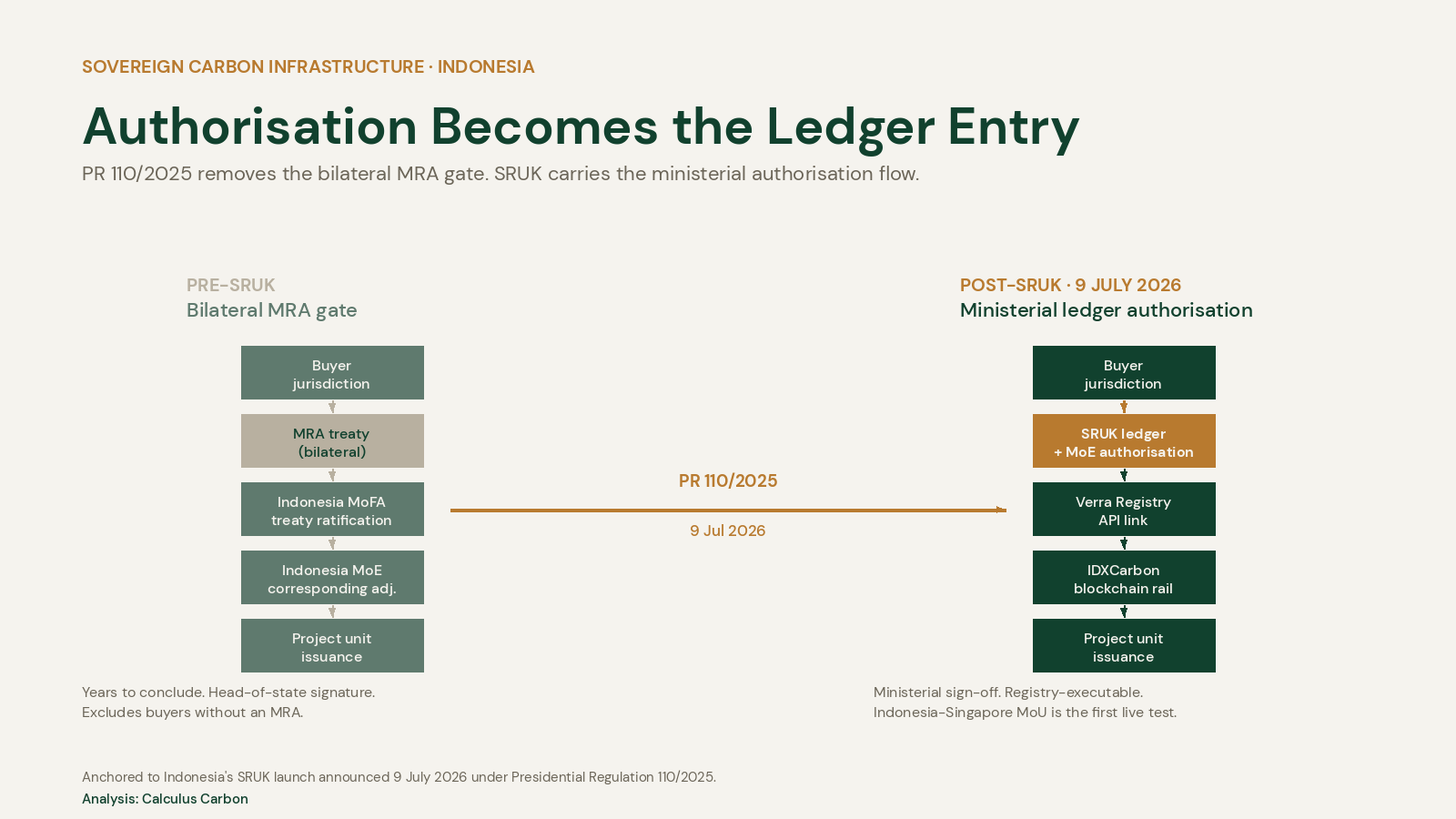

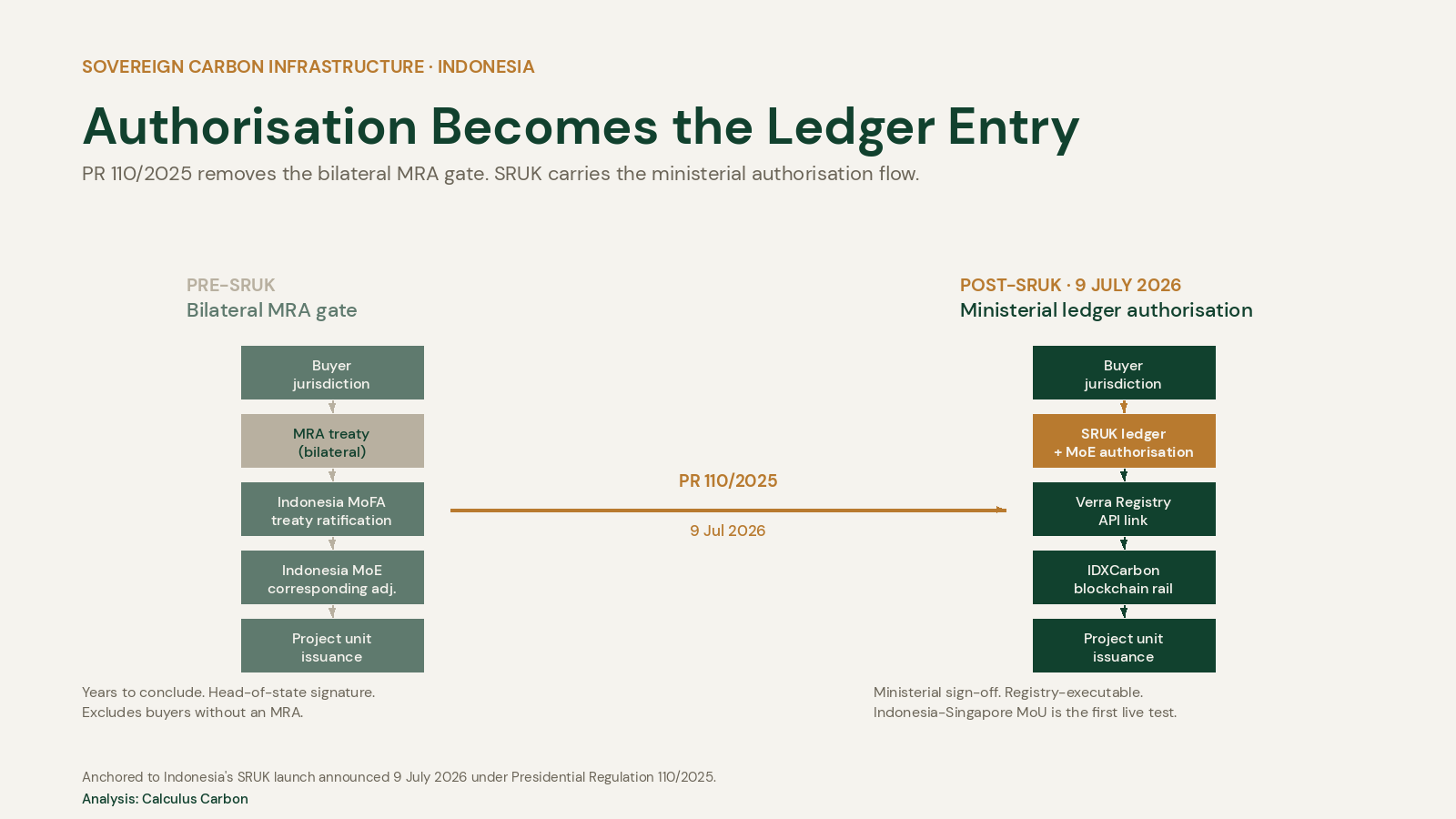

Indonesia's SRUK: Authorisation Becomes the Ledger Entry

Indonesia's Carbon Unit Registration System, launched under Presidential Regulation 110/2025, moves cross-border authorisation from bilateral treaty to ministerial ledger entry. The read for institutional capital.

Sovereign Carbon Infrastructure · Indonesia

Indonesia's SRUK: Authorisation Becomes the Ledger Entry

Indonesia's Carbon Unit Registration System, launched under Presidential Regulation 110/2025, moves cross-border authorisation from bilateral treaty to ministerial ledger entry. The read for institutional capital.

The Thesis

Indonesia launched its Carbon Unit Registration System (Sistem Registri Unit Karbon, SRUK) on 9 July 2026 under Presidential Regulation 110/2025. The launch headline is a number: roughly 31.7 million tCO2e of forestry supply being prepared by Verra for issuance across four approved concessions, at an indicative transaction value of approximately US$278 million. The structural shift underneath the number matters more.

PR 110/2025 removes the Mutual Recognition Agreement requirement that had previously gated every cross-border trade of Indonesian carbon units. Authorisation now flows through sectoral ministerial regulations, with the Minister of Environment signing off corresponding adjustments on internationally-linked trades. SRUK carries the ledger. For institutional buyers, Indonesian supply moves from paper-eligible to registry-executable. For sovereign counterparties, the corresponding-adjustment step is now procedural, not political. The Indonesia-Singapore Article 6 Memorandum of Understanding, signed the same week, is the first live test of the new architecture. This is what a country looks like when it decides to make its carbon supply bankable.1,2

What Changed on 9 July 2026

The Ministry of Environment (Kementerian Lingkungan Hidup) formally launched SRUK on 9 July 2026 as the national registry infrastructure for carbon units in Indonesia, operating under Presidential Regulation 110/2025 issued in 2025. The launch was accompanied by three concrete signals of executability.2

First, four Forest Utilisation Business Permits (Perizinan Berusaha Pemanfaatan Hutan, PBPH) were approved as the initial pipeline. Three are concession-based projects: Sumatera Merang Peatland Rewetting, Katingan Peatland Restoration, and the Mayas Project. One is a social-forestry initiative. The combined expected supply is 31,659,185 tCO2e that Verra is now preparing for issuance, with an indicative aggregate transaction value of approximately US$278 million based on the Rp5 trillion figure disclosed by Petromindo.3

Second, SRUK will API-link directly with the Verra Registry and route trades through IDXCarbon, Indonesia's carbon exchange operator, on a blockchain rail. This is not an announcement of intent. The plumbing exists.1,3

Third, Indonesia and Singapore signed an Article 6 Memorandum of Understanding the same week. That MoU is the first bilateral trade architecture designed to move Indonesian units under the new SRUK-mediated framework rather than the older MRA-based structure.6

Why the MRA Removal Is the Story

Under the framework that governed cross-border carbon trade in Indonesia before PR 110/2025, every internationally-linked transaction required a Mutual Recognition Agreement between Indonesia and the counterparty jurisdiction. MRAs are bilateral treaties. They are negotiated between foreign ministries, signed at the head-of-state level, and take years to conclude. For a project developer trying to sell Indonesian removals or reductions to a European sovereign buyer or a corporate offtaker in a jurisdiction without an MRA, the transaction was economically theoretical.

PR 110/2025 removes that bilateral gate. Authorisation now flows through sectoral ministerial regulations, meaning the Ministry of Environment (or its counterpart in a linked sector) is the executive authority. Every internationally-linked trade requires the Minister of Environment to sign off the corresponding adjustment to Indonesia's Nationally Determined Contribution accounting. That signature is administrative rather than diplomatic. The ledger of what has been authorised, adjusted, and transferred sits in SRUK.2

This is the shift the short-form ended on. Authorisation becomes a ledger entry. Not a negotiation. The reader who is a senior underwriter at an institutional allocator, a policy officer at a Development Finance Institution, or a compliance-market buyer sitting in Switzerland, Japan, or Korea will recognise the difference between "the country has signed an MoU" and "the country has an operating registry with an authorisation flow through a named ministerial process". Indonesia has moved from the first category into the second.

How the Verra Integration and IDXCarbon Routing Change the Diligence Path

Two operational features of the SRUK launch will land quickly on the diligence path institutional buyers use to underwrite emerging-market carbon supply.

The first is the Verra Registry API integration. Buyers who already run Verra-mediated pipelines have most of their compliance and verification workflow built around Verra's serial numbers, project pages, and retirement records. If SRUK API-links directly with Verra, an Indonesian unit registered in SRUK carries a machine-readable link to its Verra counterpart record. The lookup, verification, and retirement rails a buyer already knows how to use extend into Indonesian supply without a bespoke integration.

The second is the IDXCarbon routing. IDXCarbon is the exchange operator run by the Indonesia Stock Exchange (IDX) that handles domestic carbon trades under Indonesia's compliance framework. Routing SRUK-mediated internationally-linked trades through IDXCarbon on a blockchain settlement rail is a signal that the government intends Indonesian carbon units to trade like other exchange-cleared instruments. Settlement finality, audit trail, and counterparty risk are handled at the venue level rather than negotiated bilaterally on each trade.

Both features shorten the diligence cycle. A buyer who wants to trade an Indonesian removal in 2027 or 2028 will not need to build the Indonesia-specific compliance rail their team would have needed to build in 2023 or 2024. That is what "registry-executable" means in operational terms.

What the Indonesia-Singapore MoU Signals

The Indonesia-Singapore Article 6 MoU signed the same week as the SRUK launch is the first live test of the new architecture. Singapore has been building a jurisdictional demand pool for Article 6.2 units to help meet its own NDC via international transfers. Indonesia is the largest forestry-supply jurisdiction in Southeast Asia by nameplate volume. The two governments have run technical-track conversations for over three years on how to move Indonesian units to Singaporean buyers under an Article 6-compliant structure.6

The MoU is not a transaction. It is the framework under which transactions will happen. Its practical demonstration is that the SRUK-mediated authorisation flow is the pathway Singapore has been briefed on and accepted. That acceptance sets a precedent. Other jurisdictions with interest in Indonesian supply, including Korea, Japan, and Switzerland, will now negotiate against the SRUK framework rather than the older MRA framework.

The Singapore MoU is the reference point for what a "clean" Article 6.2 bilateral looks like under the new Indonesian architecture. If it clears in operational form over the next six to twelve months, the SRUK framework becomes the template for the next set of bilaterals.

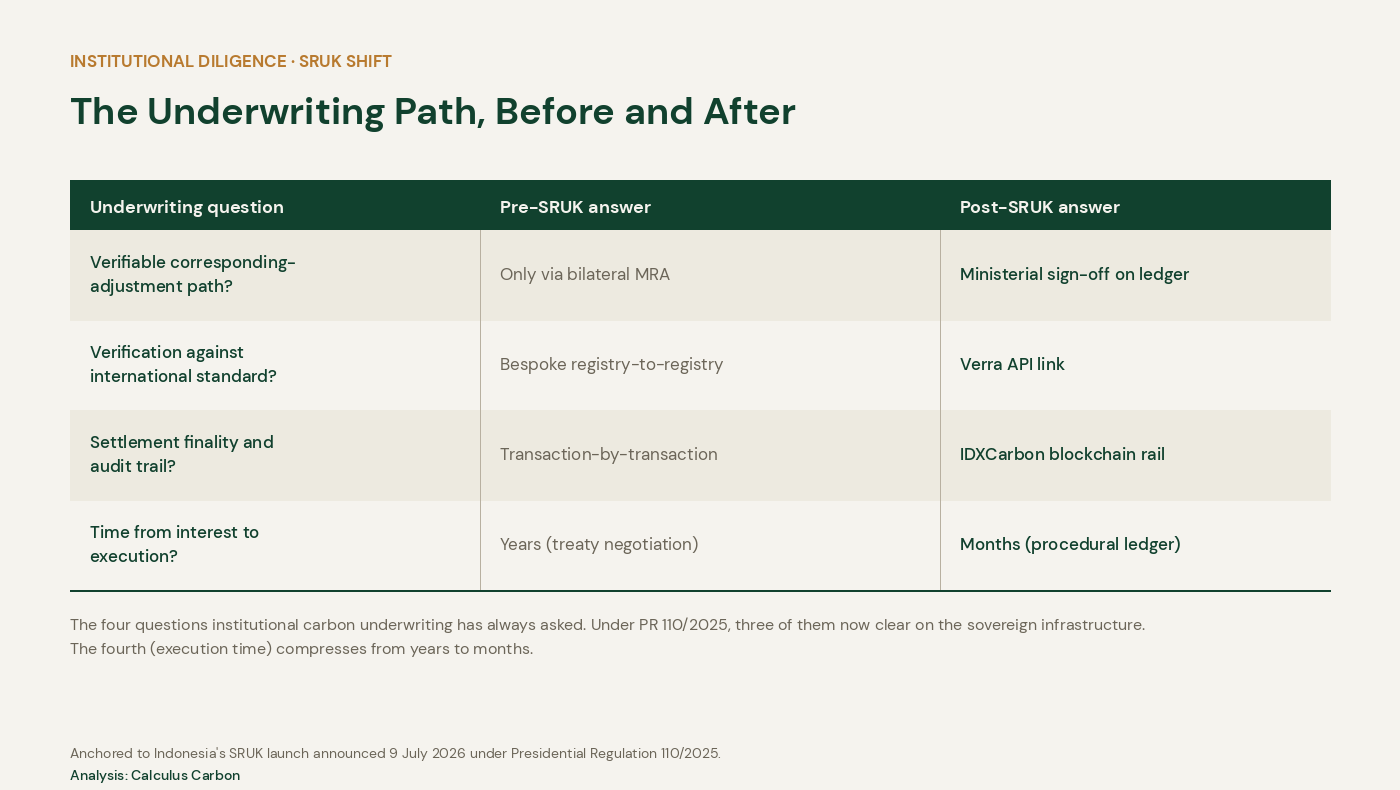

Where the Institutional Underwriting Actually Sits

The typical institutional buyer of Indonesian nature-based-solutions supply, whether a sovereign compliance-market participant, a corporate net-zero offtaker running a portfolio strategy, or a Development Finance Institution looking to underwrite bankable projects, cares about a specific set of underwriting questions. Under the pre-SRUK framework, several of those questions had no clean answer.

On the question of a verifiable corresponding-adjustment path on the seller-side NDC, the pre-SRUK framework required a signed MRA between Indonesia and the buyer's jurisdiction. Under SRUK, the adjustment is mediated by the Minister of Environment on the ledger.

On verification against a recognised international standard, the pre-SRUK framework required a bespoke registry-to-registry reconciliation. Under SRUK, verification runs via the Verra API link.

On settlement infrastructure that carries finality and audit trail, the pre-SRUK framework handled each transaction bilaterally. Under SRUK, settlement clears on the IDXCarbon rail.

None of this eliminates project-level diligence. The individual PBPH concessions still need to demonstrate additionality, baseline integrity, permanence and leakage discipline, benefit-sharing with local communities, and the operational track record that institutional underwriting requires. The SRUK launch removes a different layer of risk: the sovereign-infrastructure risk that used to sit on top of every project-level question. That is the layer of risk institutional capital has been unwilling to price, and it is the layer that has kept Indonesian supply out of institutional portfolios despite its scale.

The Read for Institutional Capital

Three implications land immediately.

For compliance-market buyers, Indonesian supply moves into the "diligence-eligible" bucket for the first time. The buyer's compliance team can now score Indonesian units against the same framework it uses for other Verra-linked emerging-market supply, with an incremental sovereign-authorisation check that runs through a named ministerial process rather than a bilateral treaty. Portfolio construction that had structurally excluded Indonesia can now include it. The size of the Indonesian pipeline, at 31.7 million tCO2e in the initial four concessions with materially more in the broader PBPH universe, is large enough to shift the geographic composition of an institutional carbon portfolio.

For sovereign buyers under Article 6.2, the corresponding-adjustment step becomes procedural. The Singapore MoU is the working example. Other bilaterals will follow the same template. The time from "government-level interest" to "transaction-level execution" compresses from years to months, and the compression sits on the seller-side infrastructure rather than on the buyer-side negotiation.

For project developers operating in Indonesia, the fundraising conversation changes. A project that carries a PBPH permit, is registered in SRUK, and has a Verra-mediated verification pathway is a materially more bankable asset than the same project would have been in 2024. Debt lenders, equity co-investors, and pre-financing partners who had priced Indonesian sovereign risk as a material discount to Southeast Asian supply can now price it closer to par.

The Frame Institutional Underwriters Will Now Carry

The move Indonesia has executed is not a treaty. It is not a headline commitment. It is a piece of registry infrastructure with an authorisation flow, an integration path to a global verification standard, and a settlement venue for internationally-linked trades. The sovereign posture has moved from negotiating each buyer relationship as a bespoke bilateral to running the buyer relationship as a ledger operation.

Authorisation becomes the ledger entry. Not the negotiation. The countries that get this right early will find that institutional carbon demand routes to them faster and prices tighter than to the countries still negotiating each buyer bilateral. Indonesia is the first significant supply jurisdiction to move the architecture. It will not be the last.

The Capital Markets Desk at Calculus Carbon will be watching what Verra prepares for issuance out of SRUK over the second half of 2026, how the Indonesia-Singapore MoU translates into the first operational trades, and which other supply jurisdictions in Southeast Asia and Africa move to comparable registry-first architectures. The read that matters for institutional capital is not the initial 31.7 million tCO2e. It is whether Indonesia has just written the template for how the next generation of sovereign carbon markets will authorise, verify, and settle.

Authorisation becomes the ledger entry. The template for the next generation of sovereign carbon markets just got written.

This piece extends the Calculus Carbon LinkedIn short-form scheduled for 16 July 2026. Analysis by the Capital Markets Desk.

Sources

- [1] Antara News, Indonesia Launches Carbon Registry to Accelerate Carbon Trading. en.antaranews.com

- [2] Kementerian Lingkungan Hidup, Indonesia Luncurkan Sistem Registri Unit Karbon Berstandar Internasional. kemenlh.go.id

- [3] Petromindo, Indonesia Launches Forestry Carbon Hub, Approves First Carbon Credit Projects. petromindo.com

- [4] Antara News, New Carbon Credit Issuance Supports Sustainability Ministry. en.antaranews.com

- [5] Nusantara DFDL, Carbon Credits Indonesia Investor Guide. nusantaradfdl.com

- [6] gCaptain, Singapore and Indonesia Sign Carbon Credits MoU, but the Real Work Is Still Ahead. gcaptain.com