Agroforestry Moved from Spot to Term: Why 10-Year Corporate Offtake Makes Working-Farm NbS Project-Financeable

Three tier-1 corporates just signed 10-year offtake on a single agroforestry project. The consequential signal is not demand, it is tenor and bankability.

Tenor Curve · Agroforestry Offtake

Agroforestry Moved from Spot to Term: Why 10-Year Corporate Offtake Makes Working-Farm NbS Project-Financeable

Three tier-1 corporates just signed 10-year offtake on a single agroforestry project. The consequential signal is not demand, it is tenor and bankability.

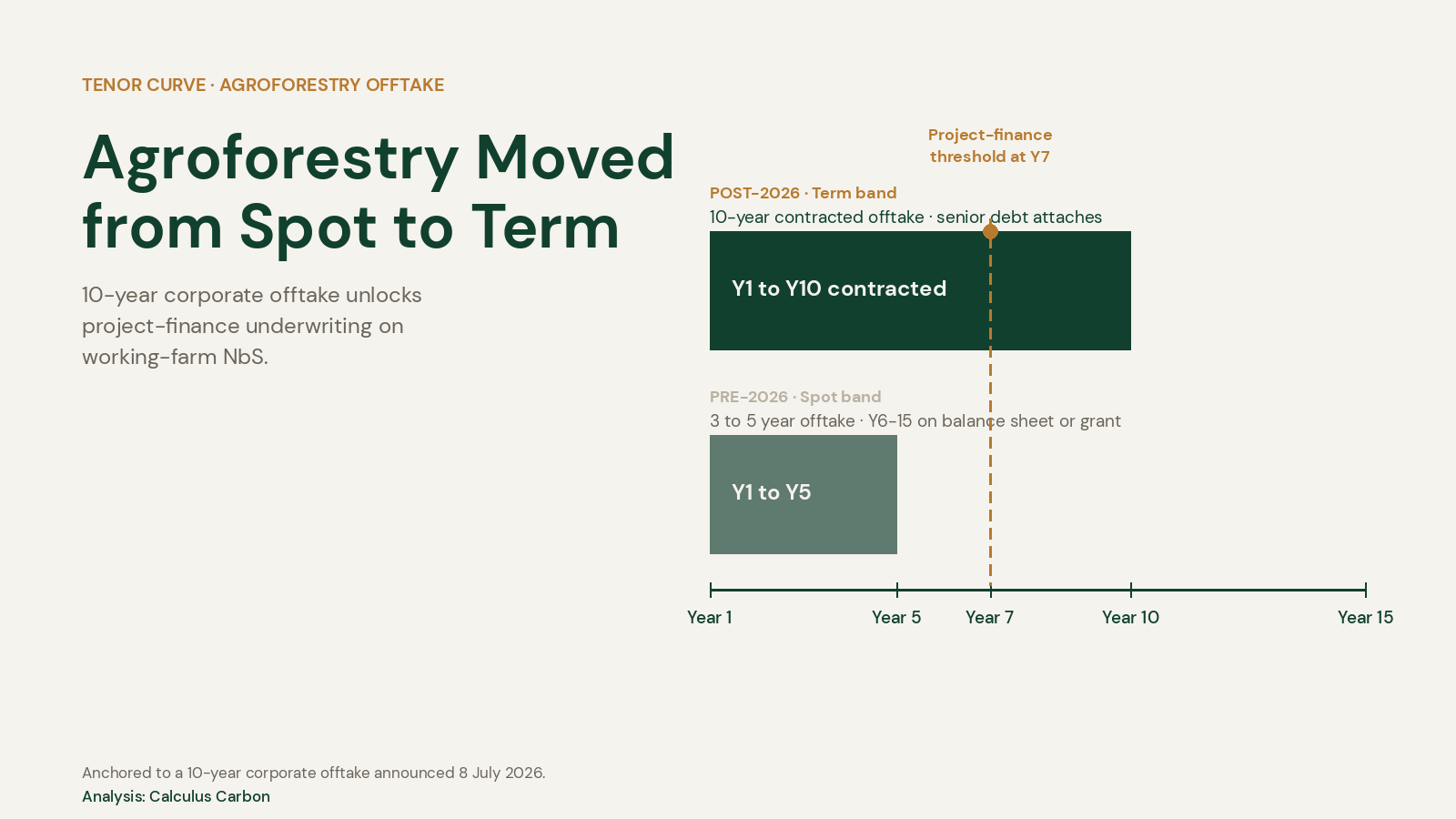

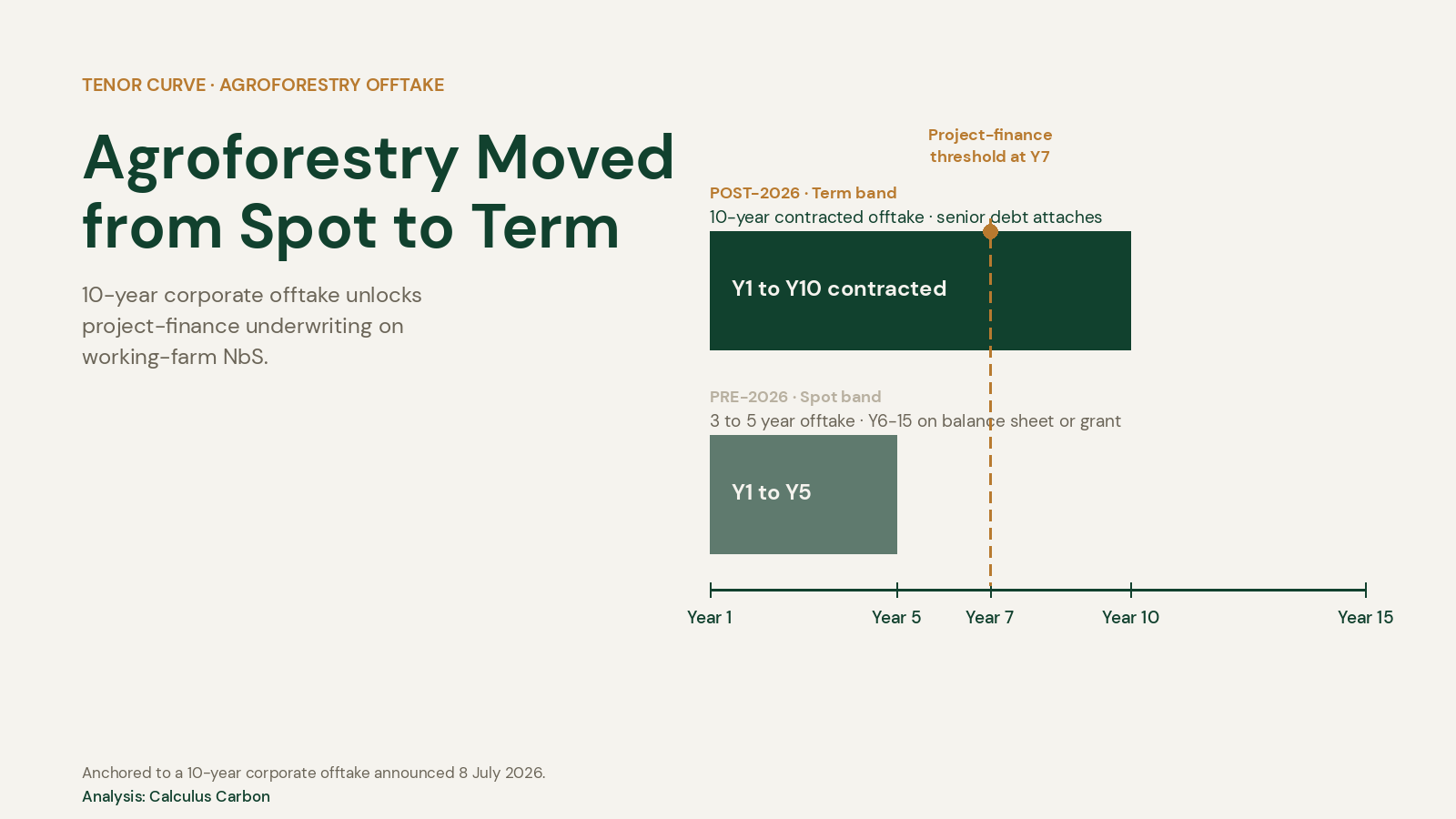

Three tier-1 corporate buyers just signed 10-year offtake on a single agroforestry project in Sulawesi. The consequential signal is not that big tech is back in the nature-based carbon market. The signal is that the tenor curve for working-farm carbon has moved from a spot band of three to five years into a term band of ten, and that shift unlocks project-finance-grade underwriting on an asset class that has, until now, been financed almost entirely off developer balance sheets.

On 8 July 2026, Thryve.Earth, a Singapore-based nature-based project developer, announced its first commercial offtake agreements. Google contracted 260,000 tonnes of nature-based carbon removal over ten years. McKinsey and Company contracted 75,000 tonnes over the same period, both through the Symbiosis Coalition. Tencent, in a separate agreement, contracted 300,000 tonnes. Combined volume: 635,000 tonnes over ten years, against 6,000 hectares of degraded land in North Sulawesi to be restored through mixed fruit, timber, and crop planting.1,2,3

The demand-side story is straightforward. Google is publicly calling this its largest carbon removal offtake to date. Tencent is publicly calling this its first nature-based offtake outside China. Both facts will be quoted in every headline for the next two weeks. The tenor story is the more useful read.

The Old Regime: Agroforestry as a Spot-Market Product

Agroforestry, as a carbon asset class, has historically been priced as a three to five year voluntary-market product. Buyers signed short-dated offtake because the buyer side of the voluntary market itself was thinly-tenored, dominated by corporate-emissions-year purchasing cycles rather than long-dated allocator mandates. Developers absorbed the resulting mismatch on their own balance sheets.

The mismatch matters because agroforestry, biophysically, is a working-farm asset. Planting a fruit, timber, or mixed-crop system in a landscape like North Sulawesi requires seven to ten years to reach mature sequestration and cash-yielding productivity. The revenue curve of the underlying project runs to fifteen or twenty years. With the offtake contract only reaching the first five years, the developer was left carrying working-capital risk on Years 6 to 15 through some combination of grant capital, philanthropic first-loss, or a very expensive equity coupon.

That structure has three consequences that show up on every project term sheet:

- Senior debt does not attach. A lender extending a 12-year loan against a revenue stream contracted for only five years is underwriting five years of contracted revenue and seven years of merchant-price risk. The blended risk profile pushes senior debt out of the stack.

- Equity IRR is priced against short-dated cash flows. Institutional equity that would otherwise underwrite a working-farm asset at a mid-teens IRR ends up demanding a high-teens or low-twenties IRR to compensate for the tenor mismatch.

- Grant capital is doing the plumbing. Philanthropic and DFI concessional windows quietly become the shock absorber for the mismatch. That capital is finite and slow-moving. The result is that agroforestry has scaled at grant-capital speed rather than institutional-capital speed.

The gating question for the asset class has therefore never been demand. It has always been tenor. The Sulawesi announcement has moved that gate.

The New Regime: 10-Year Offtake as the Pricing Benchmark

The three offtake agreements are structured over the same ten years. The offtake price is contracted, the volume is contracted, and the delivery schedule is contracted. That structure allows the project's Year 1 to Year 10 revenue stack to be sized at contracted prices. Once revenue is contracted, senior debt can be attached to it.

That, in turn, changes the project-finance arithmetic on the entire agroforestry pipeline. A project that only concessional or philanthropic capital would previously underwrite becomes, structurally, a project that a mainstream infrastructure debt fund or DFI project-finance window can underwrite. Not because the project itself changed, but because the revenue stack the lender is looking at got seven years longer.

The critical detail is that the ten-year tenor was set by the buyer at RFP stage, not negotiated at the project level. Symbiosis Coalition's public RFP guidance to developers explicitly requested a ten-year offtake proposal, with the option to propose fifteen, twenty, or thirty years. Symbiosis's own reporting on the first RFP disclosed that 185 projects proposed a collective 180 million tonnes over ten years across 6.6 million hectares, an area larger than Costa Rica.4 The tenor of the tenor was set by the buyer. The whole pipeline it triggered is being priced against that tenor.

Symbiosis itself is not a one-project actor. It is a 20 million-tonne advance market commitment established in 2024 by Google, Meta, Microsoft, and Salesforce, with a stated goal of contracting up to 20 million tonnes of high-quality nature-based carbon removal by 2030.5 That headline number is often reported as a demand-side story. Reported that way, the number is impressive. Reported through the tenor lens, the number is transformative: 20 million tonnes contracted on ten-year term at RFP stage sets a pricing benchmark that every other agroforestry, reforestation, and mangrove developer in the pipeline gets to point at when they walk into their next capital-raise.

How the 10-Year Tenor Changes the Capital Stack

| Layer | Pre-2026 spot regime (3 to 5 year offtake) | Post-2026 term regime (10 year offtake) |

|---|---|---|

| Revenue certainty | Years 1 to 5 contracted; Years 6 to 15 merchant | Years 1 to 10 contracted; Years 11 to 15 merchant |

| Senior project-finance debt | Rarely attaches (five years of merchant risk after contracted revenue) | Attaches cleanly at Year 1 with tail coverage on Years 11 to 15 |

| Equity IRR pricing | High-teens to low-twenties to compensate for tenor mismatch | Mid-teens; equity underwrites operational and outcome risk, not tenor risk |

| Developer working capital | Balance-sheet, grant, philanthropic first-loss | Structured loan against contracted revenue |

The table is simplified and every project has its own idiosyncrasies. The direction of travel is not simplified. Contracted revenue that runs ten years lets a project-finance underwriter build a real debt-service coverage ratio. Once a coverage ratio can be built, the developer stops paying an equity coupon on working capital that should have been debt.

Two Case Studies, One Direction of Travel

The Sulawesi Thryve.Earth transaction is the anchor case. Symbiosis Coalition has publicly described the project as its first agroforestry deal and its third carbon-removal transaction to date.4 Thryve.Earth itself has said the offtake commitments will help it raise financing for the project by providing volume and price certainty, which is the same language a project-finance-financeable developer would use.3 The project targets a 6,000-hectare planting programme with the potential to expand to 10,000 hectares.6

The second case, adjacent rather than identical, is worth naming as a counter-example. Working-farm NbS in commodity-offtake regimes such as cocoa, coconut, cashew, and paulownia have historically financed themselves against physical commodity offtake, with the carbon-credit revenue stack sitting as an ancillary line on the term sheet. In those cases, tenor was already long, but the load-bearing revenue was the commodity, not the carbon. The Symbiosis-style RFP does something different: it treats the carbon revenue itself as the primary underwriting stack, and it sizes that carbon revenue at a tenor commodity buyers would recognise. That collapses the historical gap between commodity-offtake NbS and pure-carbon NbS: the same project-finance underwriting technology now applies to both.

The Implication for Allocators, Sponsors, and Developers

For allocators, the read is that the natural-capital market has crossed a structural threshold on tenor. The next twelve months will produce a wave of agroforestry and reforestation projects priced against the Symbiosis benchmark. Institutional debt investors who have historically avoided this segment because it was priced as venture-adjacent equity now have an entry point at senior debt.

For sponsors, the read is that the equity coupon on working-farm NbS is about to compress. An asset class where the equity investor was previously compensated for tenor risk will now compete on operational and outcome risk. Sponsors who can underwrite the operational side (land tenure, community consent, planting protocols, outcome measurement) will earn a market equity return without needing to price in a tenor premium.

For developers, the read is that the RFP-stage tenor is the new pricing anchor. A ten-year offtake proposal is the base case a serious institutional buyer expects to see. Developers who propose five-year offtake in the current environment are pricing themselves out of the buying pool.

The Structural Read

The demand side of the story is easier to write. The tenor side is more useful to underwrite. With three tier-1 corporates setting the reference tenor at ten years on a single project, and with the coalition behind them having already asked 185 other projects to propose the same tenor, the whole agroforestry pipeline gets to price against that curve. Term-out becomes the base case on cocoa, coconut, cashew, paulownia, and the wider set of working-farm NbS projects that have been stuck at spot-market pricing.

Agroforestry moved from spot to term. The tenor gate on working-farm NbS just cleared.

This piece extends the LinkedIn post published 14 July 2026. Analysis by Neelesh Agrawal.

Sources

- [1] Thryve.Earth, Free, Prior and Informed Consent (FPIC) in Nature-Based Carbon Projects. thryve.earth/knowledge-hub

- [2] Google, Thryve.Earth Agroforestry Offtake Announcement. blog.google

- [3] ESG Today, Google, McKinsey, Tencent Sign Large-Scale Nature-Based Carbon Removal Deals. esgtoday.com

- [4] Symbiosis Coalition, Unlocking Restoration at Scale: Early Insights from the First RFP. symbiosiscoalition.org/perspectives

- [5] Symbiosis Coalition, Home. symbiosiscoalition.org

- [6] Thryve.Earth, North Sulawesi Project. thryve.earth/project/north-sulawesi