Streamlined Energy and Carbon Reporting (SECR): Deciphering the Mandatory Reporting Framework

As the world grapples with the urgent need to combat climate change, governments and organizations are increasingly turning to regulatory frameworks to drive sustainability efforts. One such framework gaining prominence is the Streamlined Energy and Carbon Reporting (SECR) in the United Kingdom (UK). In this article, we delve into the intricacies of SECR, exploring its origins, requirements, reporting mechanisms, and exemptions, while also discussing its potential to catalyze organizational decarbonization efforts.

Understanding SECR: Unraveling the Framework

The Streamlined Energy and Carbon Reporting (SECR) framework, implemented on April 1st, 2019, represents a significant shift in the landscape of sustainability reporting for large organizations operating in the United Kingdom (UK). This mandatory reporting framework marks a departure from its predecessor, the Carbon Reduction Commitment (CRC) Energy Efficiency Scheme, which predominantly centered around taxation reporting. SECR, on the other hand, adopts a more comprehensive approach, encompassing not only the disclosure of greenhouse gas (GHG) emissions but also the organization's energy efficiency endeavors.

Background and Rationale:

The transition from CRC to SECR reflects a broader global trend toward enhancing corporate transparency and accountability in environmental stewardship. With mounting concerns over climate change and its far-reaching implications, governments and stakeholders are increasingly demanding greater visibility into organizations' carbon footprints and efforts to mitigate environmental impact. SECR emerges as a response to these imperatives, seeking to streamline reporting requirements while driving tangible progress toward sustainability goals.

Key Objectives and Scope:

At its core, SECR aims to promote transparency, accountability, and action on energy consumption and carbon emissions among large UK organizations. By mandating reporting on both energy usage and GHG emissions, SECR provides stakeholders with a comprehensive overview of an organization's environmental performance. Unlike CRC, which focused primarily on taxation and operational aspects, SECR adopts a more holistic perspective, emphasizing the importance of energy efficiency initiatives in reducing emissions and driving long-term sustainability.

Differentiating Features:

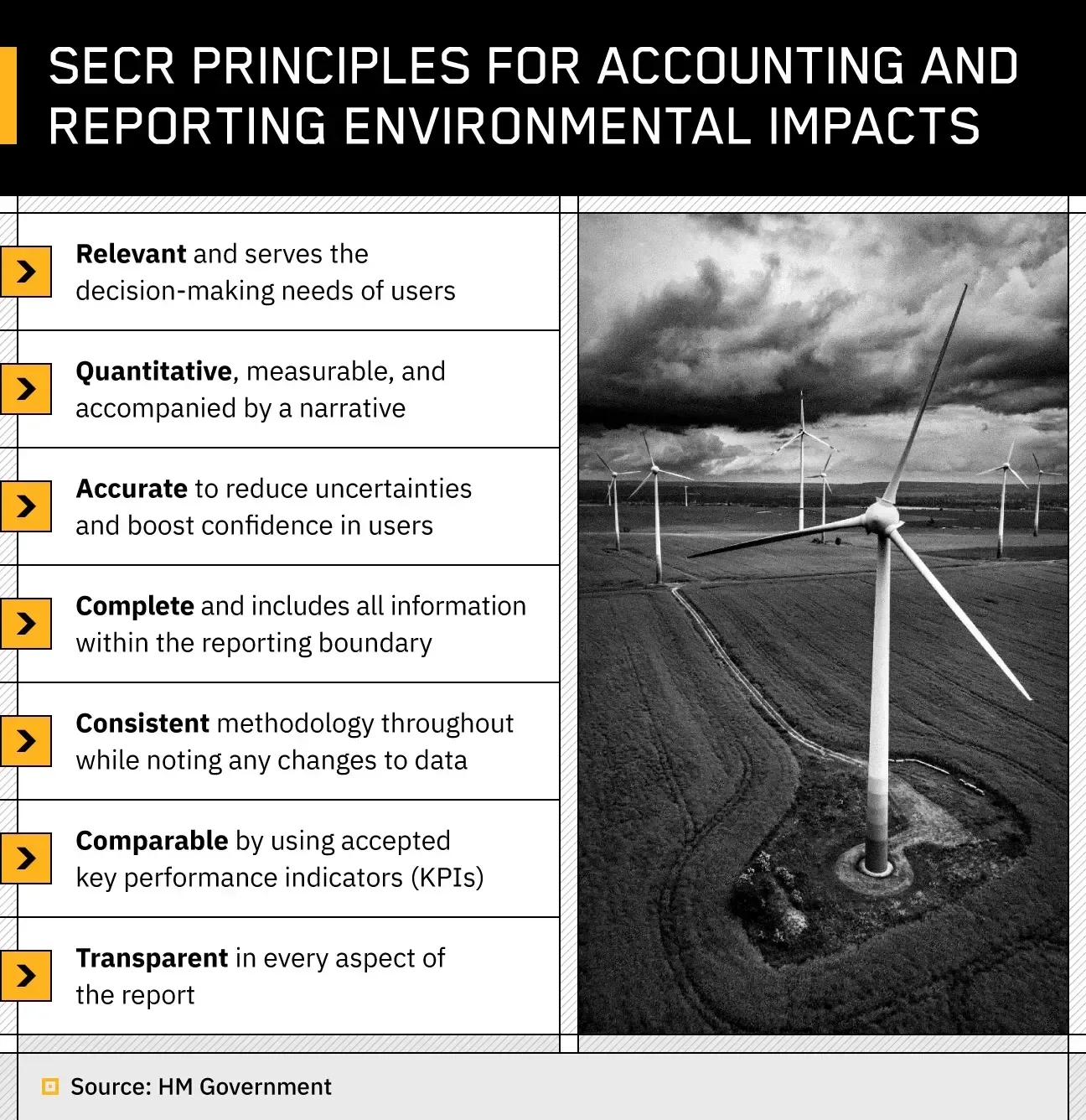

One of the distinguishing features of SECR is its emphasis on narrative reporting and intensity metrics. In addition to disclosing raw energy usage and emissions data, organizations are required to provide a narrative description of the measures undertaken to improve energy efficiency over the reporting period. This narrative component adds depth and context to the reported data, enabling stakeholders to gain insights into the organization's sustainability strategy and progress.

Furthermore, SECR mandates the calculation and disclosure of intensity ratios, which serve as a benchmark for evaluating an organization's emissions performance relative to its business metrics. By comparing emissions data with relevant business indicators such as revenue or floor space, intensity ratios provide valuable insights into the efficiency of an organization's operations and its progress toward emission reduction targets.

Implications and Benefits:

The introduction of SECR has profound implications for organizations across various sectors. By requiring mandatory reporting on energy and carbon emissions, SECR compels organizations to prioritize sustainability and integrate environmental considerations into their business strategies. This shift towards greater transparency and accountability not only enhances stakeholder trust but also drives innovation and efficiency improvements within organizations.

Moreover, SECR offers a range of benefits beyond compliance. By providing stakeholders with comprehensive insights into an organization's environmental performance, SECR enables informed decision-making and fosters dialogue on sustainability issues. Additionally, SECR empowers organizations to identify and capitalize on opportunities for cost savings, energy efficiency improvements, and emissions reductions, thereby enhancing their competitiveness in a rapidly evolving marketplace.

Who Needs to Report? Demystifying the Scope

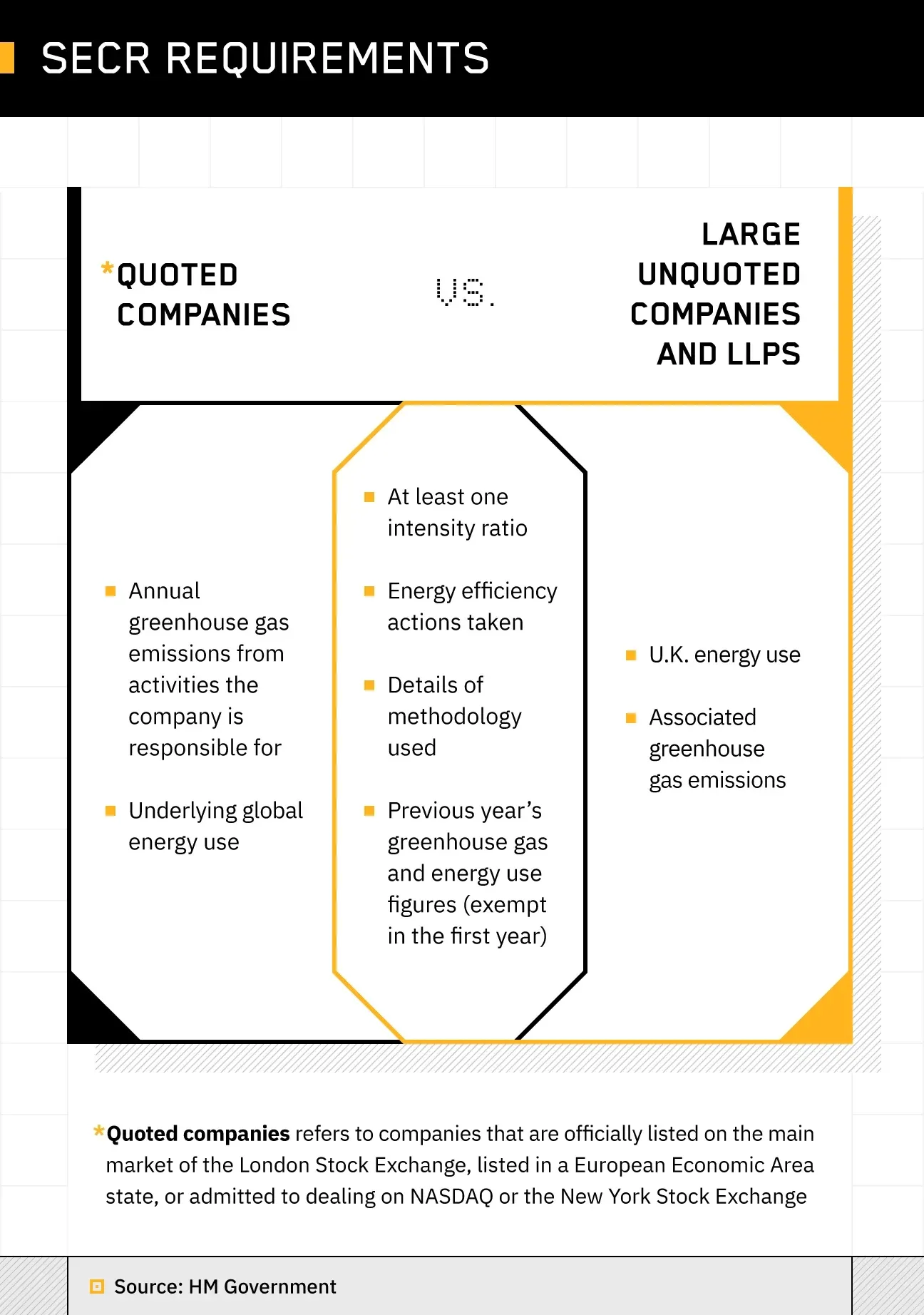

SECR applies to a wide spectrum of entities, including quoted companies, large unquoted companies, and large Limited Liability Partnerships (LLPs). Quoted companies, already obligated to comply with greenhouse gas reporting regulations, are mandated to report their global scope 1 and 2 emissions, along with chosen intensity ratios.

On the other hand, unquoted large companies and LLPs need to report their UK energy usage and associated emissions, along with at least one intensity metric.

Calculating and Reporting to SECR: Navigating the Requirements

Compliance with SECR necessitates meticulous reporting of energy usage, GHG emissions, and intensity metrics for the current and previous financial years. The reporting scope encompasses gas, purchased electricity, and transport fuel, accompanied by a comprehensive narrative description of energy efficiency measures undertaken.

While no specific methodology is mandated, organizations are encouraged to adopt robust and transparent processes for measuring energy use and emissions.

Exemptions and Flexibilities: Exploring the Nuances

Despite its mandatory nature, SECR does offer exemptions. Organizations demonstrating low energy usage (40MWh or less over the reporting period) are exempted from compliance, albeit with a requirement to include a statement confirming their low-energy status.

Additionally, public sector entities and those undertaking public activities are exempt, although voluntary reporting is encouraged to bolster transparent ESG reporting.

The Road Ahead: Leveraging SECR for Decarbonization

SECR not only fosters transparency but also serves as a catalyst for organizational decarbonization efforts. By mandating reporting on energy usage and emissions, SECR empowers organizations to identify areas for improvement, drive efficiency gains, and ultimately, reduce their carbon footprint. Moreover, SECR's focus on narrative descriptions and intensity ratios fosters a culture of accountability and continuous improvement, paving the way for a greener and more sustainable future.

In conclusion, SECR emerges as a pivotal tool in the fight against climate change, heralding a new era of sustainability reporting and corporate accountability. As organizations navigate the complexities of compliance, they also embark on a transformative journey towards a low-carbon future, where environmental stewardship and business success go hand in hand.