Q1 2024 Voluntary Carbon Market Update: Oversupply Challenges Persist Despite Record Retirements

The first quarter of 2024 saw significant developments in the Voluntary Carbon Market (VCM), with an increase in credit issuances outpacing retirements. This has led to a further inflation of oversupply, putting downward pressure on prices. Additionally, Article 6 negotiations faced setbacks, impacting the international trade of carbon credits. Here's an in-depth analysis of the key trends and developments in the VCM during Q1 2024.

Issuance and Retirement Trends

Despite a historically large number of retirements in Q1 2024, oversupply continued to balloon as issuances rose at a faster clip. Approximately 55 million tonnes of carbon credits were retired last quarter, marking the third-highest amount ever recorded.

Graph 1: Quarterly Credit Issuances (Source: MSCI)

However, this increase in retirements was overshadowed by a significant rise in credit issuances, with 89 million credits issued during the same period.

Graph 2: Quarterly Credit Retirements (Source: MSCI)

This imbalance has resulted in a continued growth in oversupply, albeit at a slower pace compared to previous years.

Graph 3: Market Surplus continues to grow (Source: MSCI)

The increase in oversupply rose by 17% over the past year, compared to 26% in the 12 months leading up to Q1 2023.

Price Dynamics

The oversupply in the VCM has put downward pressure on credit prices, with the weighted average price across all project types standing at $4.70 in Q1.

Graph 4: Quarterly Price Dynamics (Source: MSCI)

This represents a 2% decrease from the previous quarter and a 27% drop compared to the same period last year. The long-term trend of declining prices has persisted over the past few years, with prices well below the full-year averages of $5.80 in 2023 and $8.10 in 2022.

Sectoral Trends

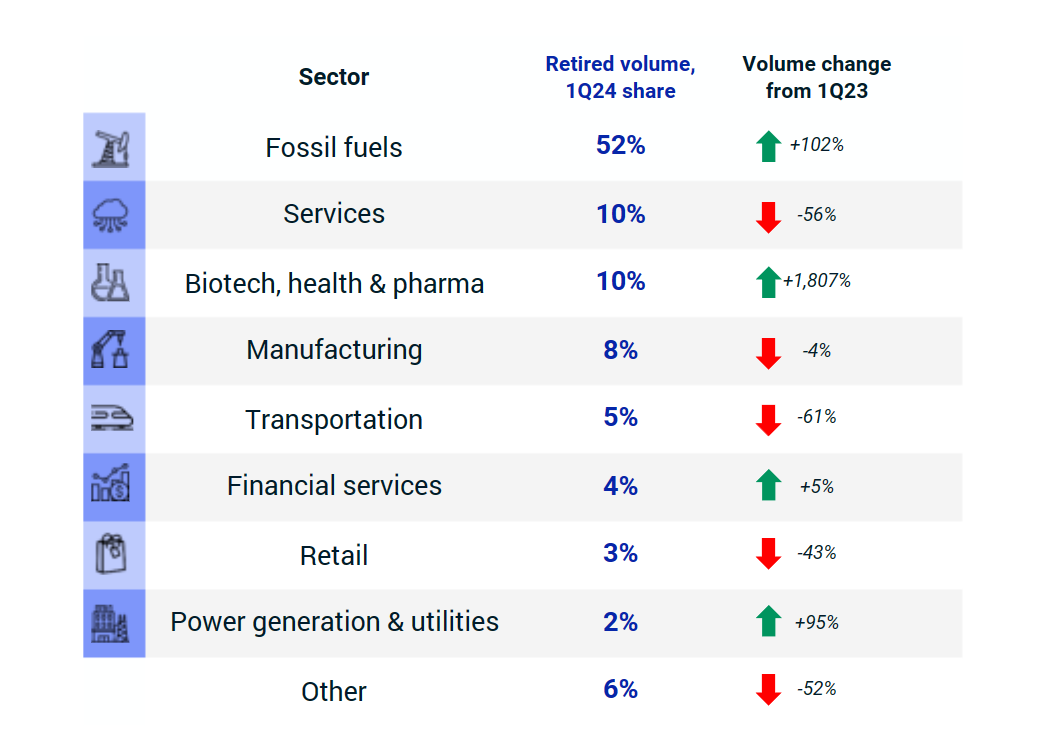

Three sectors - fossil fuels, services, and biotech, health, and pharma - accounted for three-quarters of retirements in Q1.

Table 1: Retired Volume by Sectors in 1Q24 w.r.t 1Q23 (Source: MSCI)

Fossil fuels extended its lead, driven by retirements made by European oil majors Shell and Eni. Other sectors retiring significant volumes of credits included manufacturing, transportation, financial services, retail, and power generation and utilities.

Integrity and Project Types

While the spread of credit prices across different integrity levels is continuing to reduce, integrity is gradually increasing. Land restoration projects, REDD+ projects, carbon engineering, and energy efficiency projects recorded the greatest perceived improvements in Q1 2024 compared to the same period last year.

Nature restoration and REDD+ remain the most popular project categories by retirement rate. There is also growing interest in CO2 removal (CDR) credits, which are more expensive and typically have more perceived integrity.

Article 6

There was a significant drop in the number of agreements signed for the international trade of carbon credits under Article 6.2 of the Paris Agreement in Q1 2024. While Q4 2023 saw 25 bilateral agreements signed, this fell significantly in Q1 2024 to just two deals.

This decline can partly be attributed to stalled negotiations around the terms of Article 6 at COP28 in Dubai late last year. The uncertainty over possible changes to the Article 6.2 rules has impacted the willingness of countries to enter into agreements.

Policy Developments

Several key policy developments occurred in Q1 2024 that industry stakeholders should keep an eye on. These include:

1) The first Phase 1 CORSIA-eligible credits hitting the market

2) The first programs achieving eligibility for ICVCM’s Core Carbon Principles (CCPs)

3) The EU's progress towards adopting a regulatory framework for carbon removals

Despite progress on integrity, there is ongoing scrutiny on carbon credits from academic literature, the news, and civil society groups. Efforts among standard setters to improve methodologies have been accelerated by an eagerness to align with the CCPs.

Conclusion

The Voluntary Carbon Market faced significant challenges in Q1 2024, with oversupply continuing to weigh on prices despite record retirements. The drop in the number of Article 6 agreements further added to market uncertainties. However, progress on integrity and policy developments offer some hope for addressing these challenges in the future.

Continued efforts to improve methodologies and align with best practices will be crucial for ensuring the credibility and effectiveness of the VCM in addressing climate change.