Opportunities of Indonesia in the Global Carbon Markets under Article 6

Indonesia’s Carbon Markets under Article 6 of the Paris Agreement and how it can be strengthened to meet its Net Zero targets.

Indonesia’s climate change mitigation pledges

Authored by

Erick Kariithi

Indonesia commits to meet net zero emissions target (NZE) by making a remarkable promise to contribute to curbing global greenhouse gas emissions. In aligning to the targets, it means that Indonesia needs to have a significant energy sector emissions reduction to get close to zero emissions and increase capacity in carbon removals in the forestry and land-use sectors. This calls for a transformational changes in energy, food and land-use systems. This attempt, will have targets with potential trade-offs among them, such as relating to, food security, energy security, avoiding deforestation, biodiversity conservation, freshwater use, nitrogen, and phosphorus uses, as well as competing use of land.

The apt question is how engagement in the shorter term in cooperative approaches under Article 6 of the Paris Agreement can contribute to these targets in the long term. While on the contrary, participation in cooperation approaches consideration is in relation to the current NDC.

There is therefore a need for a long-term strategy for Article 6 participation and discussions around the NDC targets in the context of LTS targets. Overall, the rules of the game especially for the private sector both in voluntary and compliance carbon markets needs clarity and the recommendations should be seen from this standpoint, as well as sovereign buyers of ITMOs.

The urgent need for a strategy that is long term for Article 6 participation

There are exciting potential opportunities for Indonesia under article 6 cooperation, including, additional financing for low-carbon development mobilization, sustainable development benefits beyond emissions reductions creation, and facilitation of technology transfer. By aiming on how Article 6 can support decarbonization goals in the Indonesian context in the long term and having a global market positioning, Indonesia could take advantage on these benefits.

Although the focus of Indonesia’s carbon market regulation (21/2022) is on how to ensure NDC achievement, the long-term objective of Indonesia’s participation in international carbon market needs a clearer formulation. It should include a very god strategy in participating in article 6 and using the Voluntary Carbon Market to both achieve NDC and contribute to NZE target.

In the worst scenario, sometimes formulation of policy around the NDC targets may threaten the NZE achievement. International cooperation limited through carbon market activities with corresponding adjustments to after the sectoral NDC target has been achieved will attract finance and technology transfer but will achieve the NZE target only if emissions continue past the duration of the cooperative approach (crediting period).

The major driving force should be that any activity around Article 6 cooperation that requires corresponding adjustment shall significantly contribute to the domestic mitigation of Indonesia. First, the clarity should be that international transfers under Article 6 and its accounting will not achieve the long-term emission reduction targets but will impact the achievement of the NDC. Second, Article 6 objectives should include specific priorities for how mitigation activities can contribute to the objectives in the long-term. Third, after the end of the crediting period, activities generating emission reductions through carbon credits need to continue generating emission reductions to achieve long-term emission reduction targets.

NDC targets and LTS targets are currently disconnected

In the scenario of Indonesia unconditional commitments increments by 37.82% from the current projected level (for the current policy scenario to align with the transition scenario), 1,217,723 ktCO2e of emissions reductions are still required to achieve NZE. Policy should broaden the scope of existing regulations so that an approach to international markets that ensures contribution to the NZE target is included and also influence the content of bilateral agreements for Article 6.2 cooperation. This may imply strategizing the use of the voluntary carbon markets.

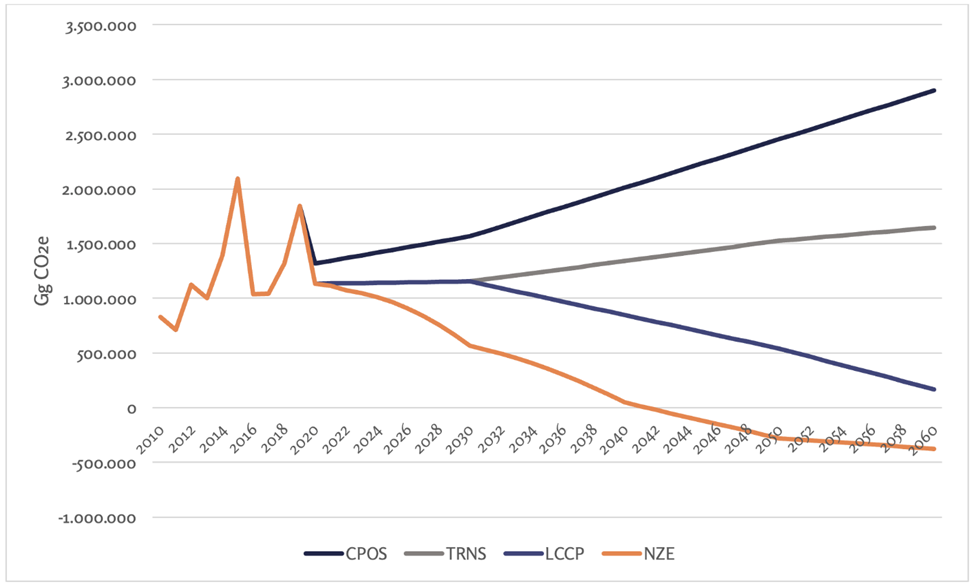

Indonesia’s LTS-LCCR applies three different scenarios to analyze long-term impacts of participation in Article 6:

- the extended unconditional commitment of NDC (CPOS),

- the transition scenario (TRNS), and

- the low carbon scenario compatible with the Paris Agreement target (LCCP).

It is challenging to achieve the net-zero emissions target by 2060 following the emissions trajectory and simulations analyzing the international carbon trading opportunities. As shown in Figure 1 below, the current policy scenario (CPOS), the transition scenario (TRNS), and the low-carbon scenario compatible with the Paris Agreement target (LCCP) all are above the net-zero pathway (NZE) for the energy and the AFOLU sectors, with only the LCCP moving downwards after 2030.

As part of the periodic update of NDCs, countries are expected to increase their level of ambition. In this five-year revision cycle, Indonesia could bridge the gap between the NDC and the NZE to allow for the CPOS scenario curve to align with the NZE. Nevertheless, by doing so and setting unconditional NDC targets that are ambitious and aligned with the net-zero target, Indonesia would most likely struggle to achieve its NDC.

When entering Article 6 cooperation, overselling is the major risk that needs to be managed. With the requirements for corresponding adjustments, Indonesia as the country transferring ITMOs (internationally transferred mitigation outcomes) may have its NDC burden increased by the volume transferred. As a result, Indonesia would be exposed to the risk of not being able to meet its NDC. In such a situation, Indonesia, like every country, has limited mitigation opportunities and the mitigation options have different costs. Indonesia would therefore have to implement more expensive mitigation activities to meet their NDCs because of corresponding adjustments.

This risk is addressed in Regulation 21/2022. The regulation states that overseas carbon trading should not occur at the expense of Indonesia realizing its NDC. This has created a view among stakeholders that Indonesia has a very restrictive policy for international carbon trade. The Ministry of Environment and Forestry has clarified that the policy is that Indonesia is open for international carbon trade.

Recommendation

The following policy recommendations could support this strategy:

1. Use of ITMOs for entities covered by compliance schemes in Indonesia clarification

Assuming that unconditional NDC targets are stringent, Indonesia may need to buy ITMOs to achieve the NDC. While this is not something to strive for, if the situation occurs, one issue will be whether the burden should fall on the government or the private sector. Should the Government be responsible for purchases to achieve sector and economy-wide targets, or could purchasing be delegated to the private sector as part of their compliance in carbon pricing schemes such as the domestic ETS. That is, if sector targets in the NDC are ambitious, and these ambitious targets are reflected in the caps for sectors subject to emissions trading schemes (cap-and-trade), then the regulated entities could be provided with the flexibility of using international offsets (ITMOs) in order to stay under their respective caps.

Providing flexibility to entities covered by the ETS is one way of easing acceptance for enlarging the ETS and provides an approach for ensuring the achievement of the NDC if the sectors covered by ETS do not perform as expected. In other words, if these entities cannot comply with their individual caps, they will need to purchase allowances. In a limited market, there may be challenges to liquidity meaning that not all entities will be able to purchase allowances from the domestic market. Under Indonesian regulations, entities can pay a tax when they emit more emissions than prescribed. However, an alternative option is to use imported ITMOs for compliance (compare flexibility of the carbon tax in Singapore). Since these ITMOs can be used towards Indonesia’s NDC, the NDC achievement is ensured despite ETS sectors not performing as expected. Furthermore, the concept of international offsets through ITMOs moves the responsibility of the purchase of ITMOs from the government to entities (companies) in the ETS.

2. Strategies for ITMO transfers, including Limitations and Quotas clarification

Quotas and limitations that can be derived from the LTS-LCCR are not defined. There are buffers set to ensure NDC implementation, but these can be returned to the project developer once the NDC is achieved. To secure NDC implementation, Indonesia could require a larger set-aside of mitigation outcomes to be counted towards its NDC target. Furthermore, ambition can be promoted by ensuring that participation in Article 6 activities contributes to the long-term goals of the Paris Agreement. For example, this could be achieved by limiting crediting periods and setting stringent criteria for crediting period renewal.

3. ITMO pricing strategy development

ITMO prices are not transparent as the market is emerging. This may continue to be the case since transactions are between sovereign states or involve companies in bilateral over-the-counter deals. Thus, there is no international market price, nor is there any demand center for ITMOs on which pricing of transactions can be based.

Indonesia may or may not have a direct role in the pricing of ITMOs. UNFCCC rules will not govern the financial flows associated with ITMO transfers and will be up to the contractual agreements of host and buyer countries, as well as any parties they authorize to participate in transactions. Regardless of the contractual arrangements, key factors that could influence the pricing of ITMOs include the following:

- The abatement cost of the specific mitigation intervention used for the Article 6 cooperation.

- The marginal cost of meeting the NDC of the host country – in other words, the cost per tCO2 of the next unit of emission reductions beyond the NDC goal.

- An international market price for ITMOs when the market is mature enough to provide this information.

- A possible premium based on the co-benefits associated with the underlying emission reduction activities. This has been the case in the voluntary carbon market in the past, and many of the Article 6 pilot activities are focused on areas with high development benefits.

One way of pricing is to consider the opportunity cost of transferring ITMOs. Corresponding adjustments create an obligation and liability for the host country since the host country’s emissions balance increases as a result of the adjustment. This has been modelled and results show that many host countries (in Southeast Asia) would need to charge more than US$25 per ton CO2e in addition to the cost of the mitigation outcome. However, the cost is specific to each NDC. It could be useful to analyze the opportunity cost specifically for Indonesia and for different NDCs under different scenarios.

Pricing can be an instrument to ensure a sustainable administration of Article 6 in Indonesia and can also be used to set aside financial resources for other purposes, such as implementing additional mitigation activities.

4. Capitalize on the opportunities from a regulated VCM (without corresponding adjustments) for achieving NDC goals.

Indonesia will have to significantly increase the ambition of future unconditional NDC targets to get closer to the net-zero pathway. To achieve this may require a significant amount of investment, perhaps beyond what it can domestically commit to. In this context Indonesia should be strategic in its participation in the voluntary carbon market (VCM) and should consider the use of the VCM to achieve the unconditional NDC. This translates into not requiring corresponding adjustments for VCM projects. Requiring authorization and corresponding adjustments for VCM activities where this is not required by the independent standard nor the buyer, may seem like an unduly restrictive policy, at least in the short-term. This does not mean that Indonesia should not impose unduly constraining regulations for the VCM in the country. Indonesia has introduced a policy on the VCM for forestry activities based on the wish to “avoid the occurrence of carbon contracts from forests unknown by the government even though carbon exploitation has occurred every year”. Indonesia could have similar requirements for other sectors.

Since the market currently is fragmented, it may benefit Indonesia to be pragmatic, but it needs to be cognizant of risks. In one scenario, Indonesia may lose out on private sector finance flow through the VCM if it applies a strict NDC accounting approach requiring corresponding adjustments in all cases. In another scenario, it may lose the interest of countries that only want to buy ITMOs from countries that have strict NDC accounting approaches. It could therefore be suggested that Indonesia’s policy context should clearly state that any emission reduction that does not include corresponding adjustments will be counted towards the NDC of the host country. With such a signal, the risk of making a specific type of claim will lie with the buyer.

5. Participation objectives in International Carbon Trade clarification

The recommendation is to use the LT-LCCR to guide Article 6 participation and not only consider the short-term NDC achievement conditions. If this is done, Indonesian stakeholders as well as carbon credit buyers will know the preferences of Indonesia in terms of technology and mitigation activity types, and they will understand the role of Article 6 in implementing the long-term strategy towards net-zero emissions 2060. Basing the participation objectives on the LT-LCCR means that technology priorities can be explicitly defined. The LT-LCCR should be used to identify technology and financing needs over time in comparison to the current situation in order to identify gaps and explore the co-benefits from mitigation action, as part of prioritizing the country’s strategy to reach net-zero emissions.

Conclusion

Moving forward, Indonesia could benefit from clarifying its carbon market framework, including optimizing the role of international carbon markets for achieving the NZE. The private sector as well as sovereign buyers of ITMOs need clear rules of the game. This is emphasized in a recent analysis by industry groups in Indonesia that also highlights the need to optimize the international carbon markets.