Insights into the Evolving Voluntary Carbon Market of 2024

From redesigning products to embracing renewable energy and implementing circular business models, companies are undertaking multifaceted approaches to reduce their carbon footprint. Let's delve into some leading strategies being employed by corporations worldwide.

In 2024, the voluntary carbon market is undergoing substantial changes, meeting crucial needs. These changes include volume growth, tech advancements, regulatory shifts, offset diversification, and greater corporate involvement. Such trends indicate a maturing market, recognized as pivotal in combating climate change globally.

2024 Projections for Supply, Demand & Price

Issuance

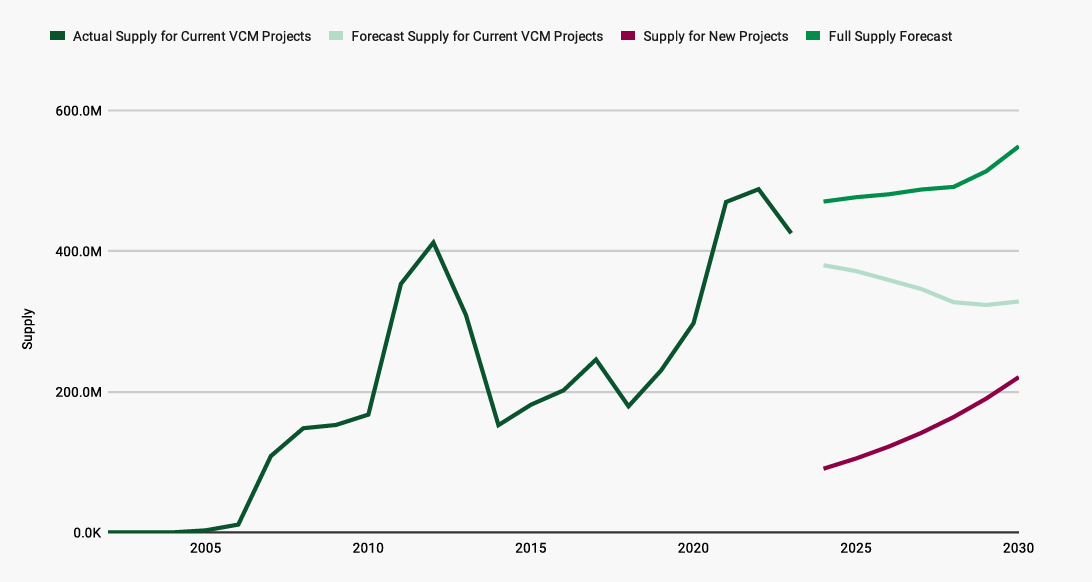

By 2030, credit supply may reach 600 million tons, with existing projects contributing up to 380 million tons and new projects adding around 210 million tons.

Graph 1: YOY Issuance Projections (in Million tonnes) (Source: Allied Offsets)

In 2024, there's expected to be a rise in issuances from new projects and a decline in supply from current projects, resulting in an overall increase in issuances, including for NBS projects.

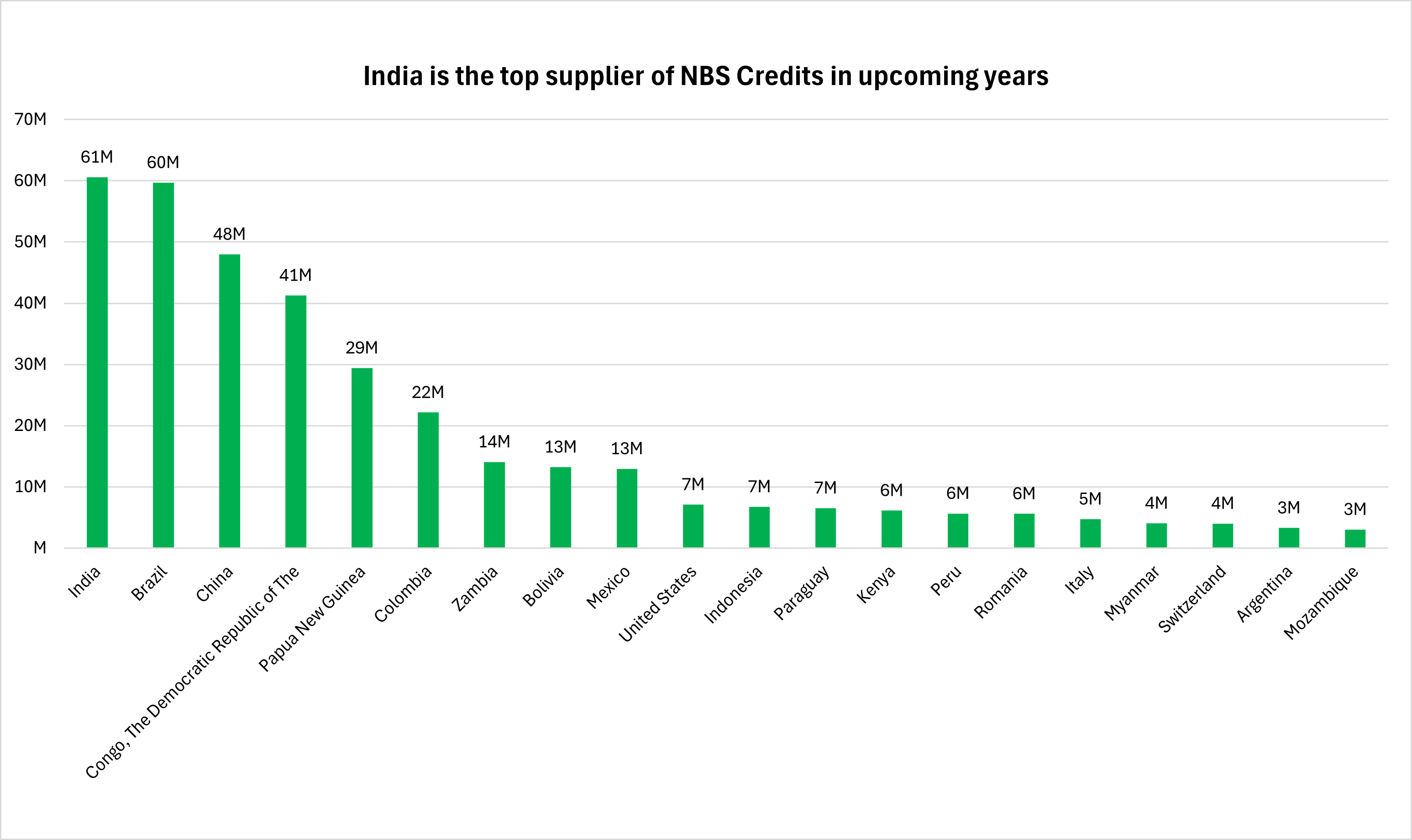

Graph 2: Comparative analysis of projected future NBS issuance supply across different countries. (in Million tonnes) (Source: Verra)

Upon reviewing the projects in Verra's pipeline, it's evident that India is poised to emerge as the largest supplier of AFLOU, projected to achieve an estimated annual emission reduction of 61 million tonnes, closely followed by Brazil.

Retirement

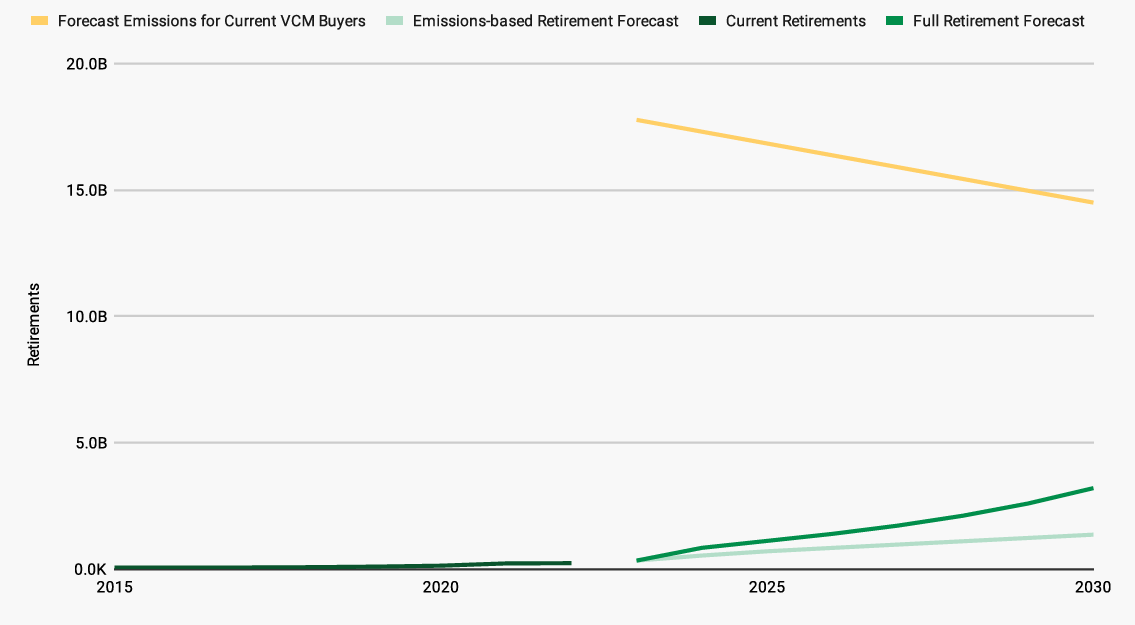

By 2030, demand from current buyers could push up to 1.5 billion tons of carbon credits, while consistent entry of new companies could potentially escalate demand to 4 billion tons annually.

Graph 3: YOY Retirement Projections (in Billion tonnes) (Source: Allied Offsets)

In 2024, a notable increase in demand for nature-based carbon credits is anticipated. Graph 11 illustrates this trend, showing rising forecasts for both total retirements and emissions-based retirements.

Price

Increasing volume and participation in the carbon credit market will impact pricing significantly. There are expectations of a moderate price increase, reflecting higher demand and better-quality offset projects, directing more funding towards impactful initiatives and fostering market growth. Currently, VCU prices are too low for effective sustainable project finance, necessitating a substantial increase.

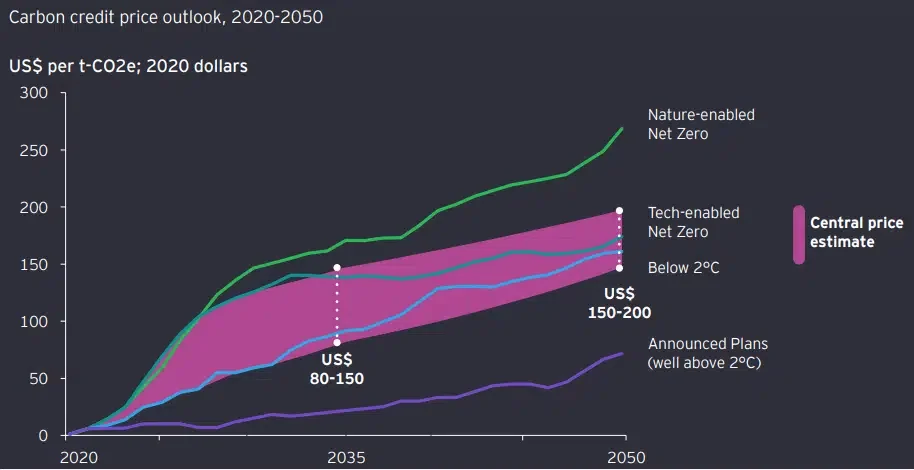

Graph 4: Price Projections

Projections indicate prices could rise from under $25/tCO2e today to $80-150/tCO2e by 2035, and further to $150-$200/tCO2e by 2050 (in real 2020 dollars). A supply-demand mismatch is also anticipated, further driving short and medium-term price increases.

Expected Trends & Outcomes of 2024

2024 has the potential to mark a turning point for the market, with expectations leaning towards a year of growth, enhanced quality, and increased prices.

- Continuation of Market Growth: A similar or increased number of unique companies (1000+) entering the VCM, fostering market stabilization and wider adoption.

- Increased Buyer Awareness: Buyers demonstrate greater awareness and maturity in credit purchases, with corporate motives surpassing marketing intentions. Expect involvement from finance, legal, and ESG departments, enriching perspectives in the VCM.

- Application of Core Carbon Principle Labels: Potential application of these labels to crediting programs, potentially leading to price increases in the market.

- Nature-based carbon credits will be prioritized: In 2024, there will be a significant surge in demand for nature-based carbon credits, particularly in the financial services sector, with over 50% seeking these credits. Organizations supporting these credits aim to reduce and remove emissions through initiatives such as landscape preservation and ecosystem restoration. This trend is fueled by heightened awareness of biodiversity conservation and consumer support for environmental protection, enhancing the brand reputations of involved companies.

- Enhanced Confidence in REDD+ Credits: Improved confidence in REDD+ credits, driven by the supply of high-quality JREDD+ credits from Costa Rica and Ghana to buyers in the LEAF coalition. Despite challenges in 2023, rainforest conservation remains a corporate priority, rendering JREDD an appealing investment option.

- COP29 & Article 6: In 2024, Article 6, especially 6.4, faces a decisive juncture, needing additional guidance before becoming operational. COP29 in Baku offers the next opportunity for Parties to finalize guidance on Article 6. Developments under both 6.2 and 6.4 will shape the potential operationalization and effectiveness of these mechanisms in boosting global mitigation efforts.

Rebuilding Trust in NBS & Insetting to Access Financing

Growing investor scrutiny for net-zero emissions alignment and tangible environmental benefits emphasizes the necessity for enhanced climate and nature-related financial reporting. Initiatives like the Glasgow Financial Alliance for Net Zero, with $130 trillion in commitments, signal a notable change in investor focus. Nature-based solutions (NBS) have gained traction as a means to bolster financial flows for carbon removal, biodiversity conservation, and social welfare. Yet, unlocking NBS's full potential demands overcoming financing hurdles.

Ways to Rebuild Trust and Increase Financing

NBS:

- Increased Investor Confidence: Mainstream investors often perceive NBS investments as high-risk due to limited examples of scalable success and currency risks, especially in frontier regions. To mitigate this, collating and sharing expert knowledge among investors, understanding how robust NBS projects can provide cash flow certainty, and implementing policies that create long-term market certainty are crucial steps.

- Reducing Perceived Risks: Systematizing existing knowledge and building consensus on guidelines and standards can address the lack of information, reducing perceived risks for mainstream investors. Lessons from traditional timberland investments can be applied, emphasizing partnerships with experts in forest management, indigenous groups, and local communities to mitigate risks and ensure successful outcomes.

- Alleviating Cash Flow Uncertainty: Diversifying investments in different sustainable forest activities, integrating natural benefits into established portfolios, and developing new valuation and business models can help alleviate uncertainty over cash flow. Additionally, policies nurturing a circular economy and providing long-term market stability through green taxonomies and end-market policies are essential.

Carbon Insetting:

What is it?

Amid the climate crisis, businesses are turning to innovative strategies like carbon insetting to bolster sustainability efforts. Unlike traditional carbon offsetting, insetting involves companies directly reducing emissions within their supply chains, offering a more targeted approach to carbon footprint reduction.

Benefits and Challenges

Insetting offers several advantages, including direct impact, cost savings, strengthened business relationships, and enhanced brand reputation. However, challenges such as implementation complexity, verification, transparency, and economic considerations must be addressed.

Nestlé's Insetting Initiatives

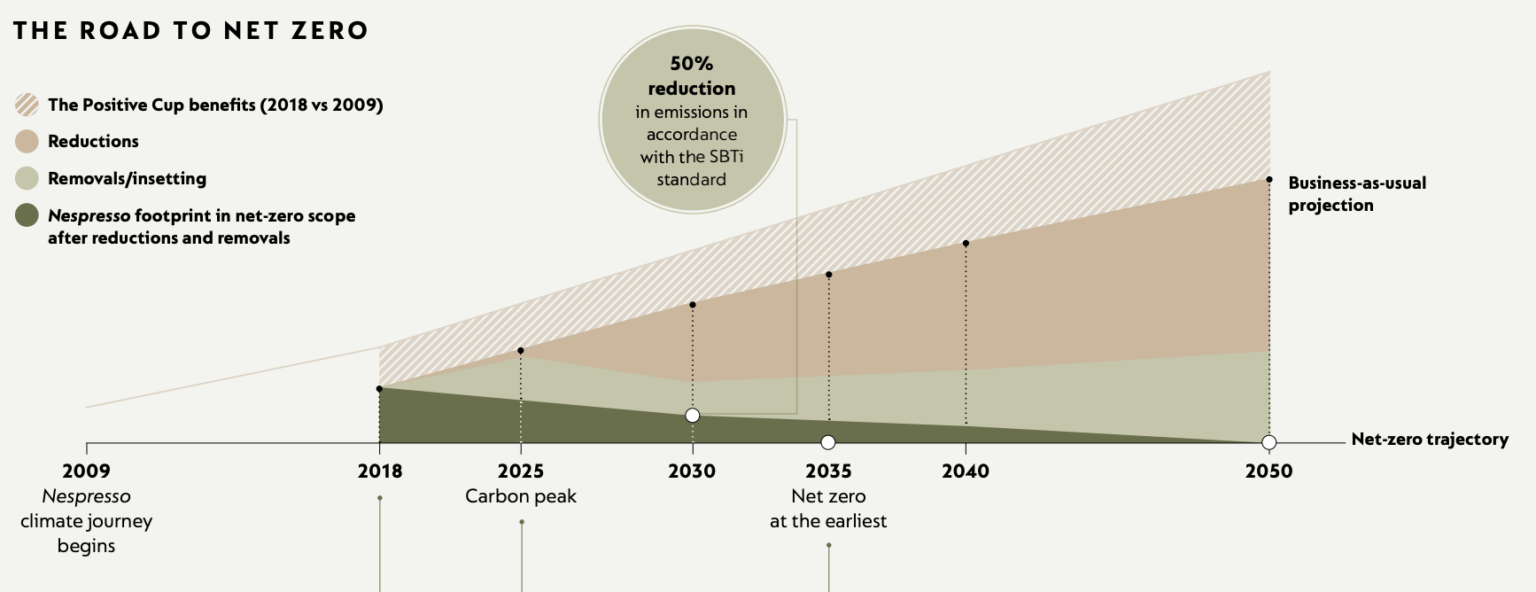

Graph 5: Role of removals and insetting in Nespresso's net zero strategy. (Source: Nespresso)

Nestlé leads in insetting, focusing on sustainable agriculture with long-term contracts in Nicaragua. Standardization, collaboration, and innovation are key for maximizing insetting's impact. Insetting offers a direct, holistic approach to emission reduction, revolutionizing corporate sustainability and contributing to global efforts.

To enhance confidence in carbon insetting and boost funding, the following strategies are imperative:

- Standardization: Establishing clear standards and guidelines for insetting is vital to ensure consistency and credibility. This will enable companies to navigate insetting complexities effectively, ensuring genuine impact.

- Partnership: Collaborative endeavors involving businesses, governments, and NGOs can amplify insetting's impact. Joint initiatives facilitate resource pooling and expertise sharing, fostering more effective and widespread insetting practices.

- Innovation: Leveraging technological advancements, such as AI-driven supply chain analytics and sustainable production technologies, is critical for advancing insetting efforts. Innovation will play a pivotal role in shaping the future of insetting initiatives.

What’s Next?

The voluntary carbon market in 2024 is undergoing significant changes, meeting the demands of the times. These changes include increased market volume, technological advancements, regulatory shifts, diversification of carbon offsets, and greater corporate engagement. This evolution reflects the market's maturity and its growing importance in combating climate change globally.

Looking ahead, these transformations indicate a future where the market becomes larger, more diverse, and integrated into broader economic and environmental strategies worldwide. While presenting opportunities, these shifts also pose challenges, emphasizing the importance of ongoing innovation, collaboration, and commitment to maintaining market integrity and effectiveness in reducing emissions.